Open Banking is a transformative concept that has revolutionized the financial landscape, bringing about increased transparency, convenience, and innovation. One prominent player in the Open Banking sphere is Revolut, a leading digital banking platform that has harnessed the power of this concept to offer its customers a seamless and interconnected financial experience. Revolut’s adoption of Open Banking has opened up a world of possibilities for its users. By securely connecting their Revolut accounts with other financial institutions, individuals can now access and manage all their financial information in one centralized location. This means no more juggling multiple apps or platforms to keep track of balances, transactions, and investments. The core principle behind Open Banking is the secure sharing of financial data between different authorized parties. Revolut, as a licensed financial institution, adheres to stringent security protocols and operates within the regulatory frameworks set by financial authorities. This ensures that users’ data and privacy remain protected throughout the Open Banking process.

What is Open Banking?

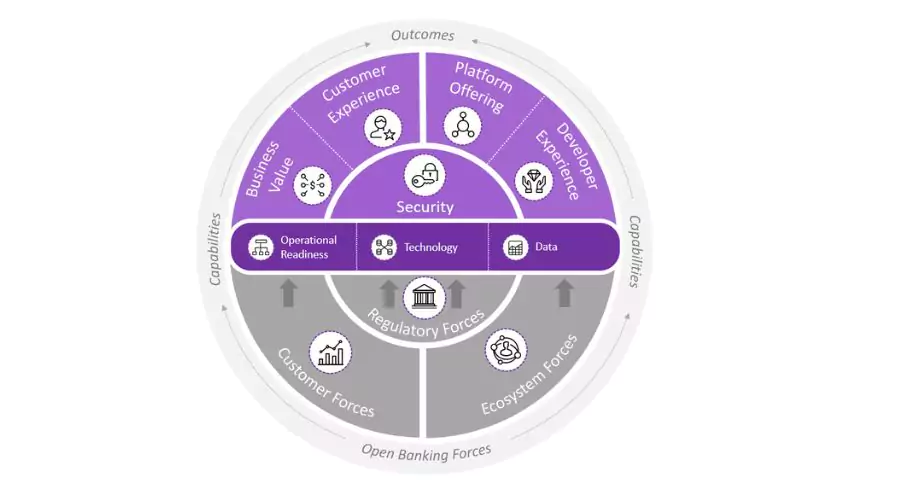

Open Banking refers to the practice of securely sharing financial data between different authorized parties, typically facilitated through the use of application programming interfaces (APIs). It allows customers to grant access to their financial information to third-party providers, enabling them to develop innovative services and products.

The Key Principles of Open Banking

Open Banking is built on several key principles:

- Consumer Consent: Customers have control over their data and must provide explicit consent for its sharing.

- Secure Data Sharing: Robust security measures are in place to protect sensitive financial information.

- API Integration: Standardized APIs facilitate seamless data exchange between institutions.

- Competition and Innovation: Open Banking fosters competition, driving innovation and the development of new financial solutions.

The Benefits of Open Banking

Enhanced Financial Transparency

Open Banking empowers customers with a comprehensive view of their financial data. By linking their accounts from different institutions, individuals can access a unified dashboard that provides a holistic overview of their finances, including balances, transactions, and investments. This transparency promotes better financial decision-making and budget management.

Convenient Account Aggregation

With Open Banking, individuals no longer need to navigate multiple banking apps and platforms. They can consolidate their financial information in a single application or platform, such as a mobile banking app, providing a streamlined and user-friendly experience. This convenience simplifies financial management, saving time and effort.

Streamlined Payments and Transfers

Open Banking enables seamless fund transfers and payments. Users can initiate transactions directly from their preferred banking platform, regardless of whether the recipient’s account is held with the same institution or another bank. This eliminates the need for manual entry and reduces the risk of errors, making transactions faster and more efficient.

Personalized Financial Services

Through Open Banking, financial institutions can access a customer’s transactional data with their consent. This enables the development of personalized services and recommendations tailored to the individual’s financial needs. From optimizing investments to suggesting cost-saving opportunities, personalized guidance helps users make informed decisions and achieve their financial goals.

Open Banking Use Cases

Account Aggregation and Financial Management

Open Banking allows individuals to aggregate and manage their accounts from various institutions in a centralized platform. Services like Revolut leverage Open Banking to provide users with a holistic view of their finances, facilitating budgeting, spending analysis, and goal tracking.

Payment Initiation and Innovation

By leveraging Open Banking APIs, businesses can develop innovative payment solutions. For instance, consumers can make payments directly from their preferred banking app, eliminating the need for traditional payment methods. This convenience and simplicity contribute to a frictionless payment experience.

Access to Financial Products and Services

Open Banking enables individuals to access a wider range of financial products and services. Third-party providers can leverage customer data to offer tailored loan options, insurance plans, or investment opportunities. This fosters competition among financial institutions and expands consumer choices.

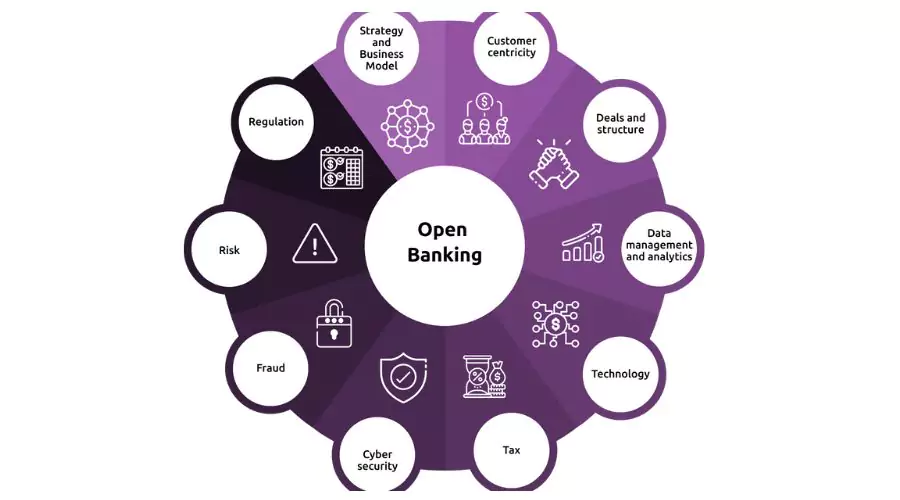

Challenges and Considerations

Data Security and Privacy

As Open Banking involves the sharing of sensitive financial information, data security and privacy are paramount. Strict regulations and robust security measures are necessary to protect customer data from unauthorized access or breaches. Financial institutions must prioritize cybersecurity and ensure compliance with relevant data protection laws.

Trust and Consent Management

Open Banking relies on customer trust and explicit consent for data sharing. Financial institutions must prioritize transparency in explaining the benefits and risks associated with Open Banking to their customers. Clear communication and user-friendly consent mechanisms are essential to build trust and maintain customer confidence.

Standardization and Interoperability

To fully realize the potential of Open Banking, standardization of APIs and data formats is crucial. Interoperability ensures seamless data exchange between different financial institutions, promoting competition and innovation. Collaborative efforts among regulators, banks, and technology providers are required to establish common standards.

The Future of Open Banking

Open Banking is still in its early stages, and its potential is far from fully realized. As technology continues to advance and regulations evolve, Open Banking will likely facilitate even more profound transformations in the financial landscape. Open Banking, coupled with emerging technologies such as artificial intelligence and blockchain, holds the promise of unlocking new opportunities and shaping the future of finance.

Conclusion

Open Banking is revolutionizing the financial industry, offering unprecedented opportunities for customers and businesses alike. Its benefits, such as enhanced transparency, convenience, and personalized services, have the potential to reshape how individuals manage their finances. While challenges around security, privacy, and standardization exist, Open Banking’s transformative impact is undeniable. As the financial ecosystem continues to evolve, Open Banking will be at the forefront, empowering consumers and driving innovation in the digital age. Follow Trendingcult for more.